![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

20 Cards in this Set

- Front

- Back

|

Books of original entry |

Business Transactions are recorded on source documents. Documents which record the business transactions in the 'books of account' include: Sales order Purchase order Invoices Credit note Debit note Goods received notes |

|

|

What is a book of original entry? |

Books of original entry are books (or computer files) in which we first record transactions. The main ones are: Sales day book Purchases day book Sales returns (or returns inwards) day book Purchases returns (or returns outwards) day book Journal Cash book Petty Cash book |

|

|

Sales day book |

The book of original entry for credit sales. It is used to keep a list of all invoices sent out to customers each day. |

|

|

Purchases day book |

The book of original entry for credit purchases. It is used to keep a list of all invoices received from creditors each day. |

|

|

Sales returns day book |

When customers return goods for some reason, the returns are recorded here. |

|

|

Purchase returns day book |

Records goods which the business sends back to its suppliers |

|

|

Cash book |

This records all transactions (receipts and payments, transfers) that go through the bank account. |

|

|

Petty Cash book |

The cash float that is kept on premises to make occasional small payments in cash for things like staff refreshments, postage stamps e.t.c. |

|

|

Ledgers (books of T accounts) |

Accounts have two sides like the cash book. These accounts are kept in a book called a ledger. There are several types of ledgers, each intended for a different type of account. |

|

|

There will be accounts for: |

Non-Current Assets Land and buildings Plant and Machinery Motor Vehicles Office Equipment Current Assets Inventories Receivables Cash Liabilities and Capital Payables Loans Proprietor's capital Expenses Purhases Rent Salaries Income Sales |

|

|

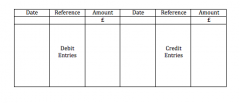

Ledger accounts presentation |

|

|

|

(Usual effects)

Asset = Debit Capital = Credit Liability = Credit Revenue = Credit Expense = Debit |

Therefore... an increase in.... Assets = debit Capital = credit Revenue = credit Expense = debit and a decrease in... Assets = credit Capital = debit Revenue = debit Expense = credit |

|

|

PRACTICE... Sally brings in £1000 extra capital during year, what do we do?

1) dr capital £1000, cr cash £1000 or 2) cr capital £1000, dr cash £1000 |

Answer = 2 |

|

|

Paul buys £5000 worth of tables & chairs via bank transfer. What do we do? |

Answer = dr Furniture £5000, cr Bank £5000 |

|

|

Paul buys £5000 worth of tables & chairs on credit from A&A ltd. What do we do? |

Answer = dr Furniture £5000, cr A&A ltd (trade payables) £5000. |

|

|

The trial balance |

Is essentially a list of all the balances on each account at the end of a period.

If you have posted correctly the dr and cr side will always balance.

If they do not, try halving the figure it's out by, and finding a posting for that amount... |

|

|

Carriage expenses |

Carriage in = add on to purchases in cost of goods sold

Carriage out = classed as expenses in bottom of income statement |

|

|

Returns in and returns out |

Returns outwards = take total off of purchases During year: dr relevant suppler, cr returns outward Returns inwards = take total off of sales during year: dr returns inward, cr relevant customer acct

|

|

|

Drawings |

Cash Drawings = dr drawings, cr bank

Goods taken for personal use = dr drawings, cr purchases |

|

|

Discounts |

Discounts allowed = classed as expense in income statement during year: dr discounts allowed, cr relevant customer Discounts received = add on as other income under gross profit during year: dr relevant suppler (payables), cr discounts received |