![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

29 Cards in this Set

- Front

- Back

|

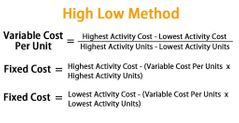

High Low Method - Formula for VC - Formula for FC |

|

|

|

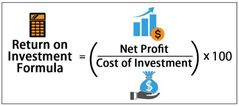

ROI Formula |

|

|

|

Residual Income Formula |

RI = Profits - (Capital Employed x Cost of Capital %) |

|

|

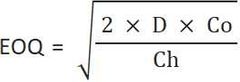

Economic Order Quantity (EOQ) Formula |

EOQ = √(2 CD) / H EOQ = √2x Cost of one order x Estimated usage / Cost of holding one unit |

|

|

Marginal Costing Inventory Valuation |

Valued at Variable production cost only (No overheads) |

|

|

Absorption Costing Inventory Valuation |

Inventory is valued at full production cost (including fixed overheads) |

|

|

Cash Operating Cycle Formula |

Aggregated - Trade payables ('Suppliers credit period') = Cash operating cycle |

|

|

Working Capital Questions |

Step 1 - Reduction = Annual credit sales (X / 360) Step 2 - Discount allowed (disc% x annual credit sales) Step 3- Profit - Cost = difference |

|

|

Contribution Formula |

Contribution = Sales price - Variable cost |

|

|

Breakeven Formula (units) |

BEP (Units) = Total fixed costs / Contribution per unit |

|

|

Margin of Safety formula |

Margin of Safety = Expected sales volume - Breakeven sales volume I.e Margin of Safety = Actual cost - Budgeted Cost |

|

|

Average Inventory Period Ratio |

Av. Inventory Period = Average Inventory / Cost of Sales x 365 |

|

|

Inventory Turnover Ratio |

(No 365!) |

|

|

Receivables collection period |

Av. Collection period = Average Receivables / Sales Revenue x 365 days |

|

|

Payables payment period |

Av. Payables period = Average Payables / Cost of sales x 365 days |

|

|

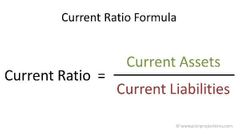

Current Ratio Formula |

|

|

|

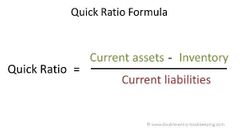

Quick Ratio Formula |

|

|

|

Breakeven Point Formula |

Breakeven Point = Fixed costs / Contribution Ratio |

|

|

Breakeven Sales Formula |

Breakeven Sales = Budget sales - Margin of Safety |

|

|

Breakeven Sales Volume Formula |

Breakeven Sales Volume = Total FC / Contribution per unit |

|

|

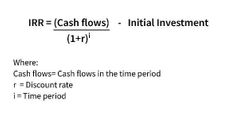

Internal Rate of Return (IRR) Formula |

|

|

|

Discounted Payback period |

Payback period using discounted values |

|

|

Optimum Transfer Price Formula |

Optimum TP = External market price - Cost savings with internal transfer |

|

|

Variable costs Formula |

VC = Sales Revenue - Contribution |

|

|

Profit formula |

Profit = Contribution - Fixed costs |

|

|

Calculating Prime Cost |

Selling Price Less: Profit mark-up Total cost Less: Overhead = Prime Cost |

|

|

Calculating Sales Revenue |

Sales Revenue x Increase % |

|

|

Calculating number of units sold |

Number of units = VC total / VC per unit |

|

|

Profit Margin Formula |

Profit Margin = Profit / Sales Revenue x 100% |