![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

32 Cards in this Set

- Front

- Back

|

An Abiding Belief in Book Value as the Best Estimate of Value: |

Accounting estimates of |

|

|

A Distrust of Market or Estimated Value |

When a current market value exists for an |

|

|

A Preference for under estimating value rather than over estimating it |

When there is |

|

|

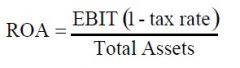

Return on Assets (ROA) |

The return on assets (ROA) of a firm measures its operating efficiency in generating profits from its assets, prior to the effects of financing.

|

|

|

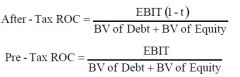

Return on Capital (ROC) |

Useful measure of return relates the operating income to the capital invested |

|

|

Return on Equity (ROE) |

Return on equity (ROE) examines profitability from the perspective of the equity investor by relating profits to the equity investor (net profit after taxes and interest expenses) to the |

|

|

Current Ratio |

The current ratio is the ratio of current assets (cash, inventory, accounts receivable) to its current liabilities (obligations coming due within the next period). |

|

|

Quick Ratio |

The quick or acid test ratio is a variant of the current ratio. It distinguishes current assets that can be converted quickly into cash (cash, marketable securities) |

|

|

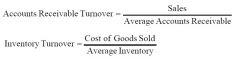

Turnover ratios |

Turnover ratios measure the efficiency of working capital management by looking at the relationship of accounts receivable and inventory to sales and to the cost of goods |

|

|

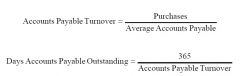

Turnover ratios (2) |

similar pair of ratios can be computed for accounts payable, relative to purchases. |

|

|

Interest Coverage |

The interest coverage ratio measures the capacity of the firm to meet interest payments from pre-debt, pre-tax earnings. |

|

|

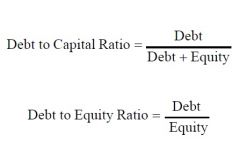

Debt ratio |

Debt ratios measure the capacity whether the Company can pay the principal on outstanding debt |

|

|

Differences in accounting standards and practices |

Differences in accounting standards across countries affect the measurement of |

|

|

Why diversification reduces or, at the limit, eliminates firm specific risk |

Each investment in a diversified portfolio is a much smaller percentage of that portfolio than |

|

|

Portfolio (expected return, variance in return) |

The expected returns and variance of a two-asset portfolio can be written as a function of these inputs and the proportion of the portfolio going to each asset. |

|

|

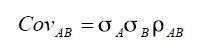

Portfolio (covariance) |

The higher the correlation in returns between the two assets, the smaller are the potential benefits from diversification |

|

|

CAPM assumptions |

- there is no transaction cost; - all assets are traded and investments are infinitely divisible; - everyone has access to the same information - there exists a riskless asset, where the expected returns are known with certainty - investors can lend and borrow at the same riskless rate to arrive at their optimal allocations |

|

|

Beta formula |

|

|

|

Arbitrage Pricing Theory (APT) |

APT- is an alternative of CAPM based on the law of one price Ross (1976) - uses less restrictive assumptions than CAPM - require than return on any stock be linearly related to a set of indexes (multi-indexes model) - it doesn't tell us what the indexes should be (for CAPM - return on market) |

|

|

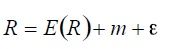

APM 2 types of risks |

R is the actual return, E(R) is the expected return, m is the market-wide component of unanticipated risk and e is the firm-specific component |

|

|

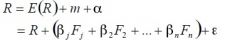

APM - market risk |

The CAPM assumes that market risk is captured in the market portfolio, whereas the arbitrage pricing model allows for multiple sources of market-wide risk and measures the sensitivity of investments to changes in each source. |

|

|

APM - market risk (formula) |

bj = Sensitivity of investment to unanticipated changes in factor j |

|

|

Multi-factors models |

Multi-factor models, like the arbitrage pricing model, assume that market risk can be captured best using multiple macro economic factors and betas relative to each. Unlike the arbitrage pricing model, multi factor models do attempt to identify the macro economic factors that drive market risk. |

|

|

Differentiating between Rewarded and Unrewarded Risk |

Risk that is specific to investment (Firm Specific) - Can be diversified away in a diversified portfolio 1. Each investment is a small proportion of portfolio; 2. Risk averages out across investments in portfolio Risk that affects all investments (Market Risk) - Cannot be diversified away since most assets are affected by it. The marginal investor is assumed to hold a “diversified” portfolio. Thus, only market risk willbe rewarded and priced |

|

|

Measuring Market Risk - The CAPM |

If there is Market Risk = Risk added by any investment Beta of asset relative to Market portfolio (from |

|

|

Measuring Market Risk - The APM |

If there are no arbitrage opportunities |

|

|

Measuring Market Risk - Multi-Factor Models |

Since market risk affects most or all investments, it must come from macro economic factors. |

|

|

Measuring Market Risk - Proxy Models |

In an efficient market, differences in returns Equation relating returns to proxy variables (from a regression) |

|

|

Critique of APM and Multi-factors model |

Extension to multiple factors does become more of a problemwhen we try to project expected returns into the future, since the betas and premiums of each of these factors now have to be estimated. Because the factor premiums and betas are themselves volatile, the estimation error may eliminate the benefits that could be gained by moving from the CAPM to more complex models. |

|

|

Critique of Proxy models |

The regression models that were offered as an alternative also have an estimation problem, since the variables that work best as proxies for market risk in one period (such as market capitalization) may not be the ones that work in the next period. |

|

|

The Determinants of Default Risk |

The default risk of a firm is a function of two variables. The first is the firm’s capacity to generate cash flows from operations and the second is its financial obligations – including interest and principal payments. The default risk is also affected by the volatility in these cash flows |

|

|

Bond Ratings |

The most widely used measure of a firm's default risk is its bond rating, which is generally assigned by an independent ratings agency. The two best known are Standard and Poor’s and Moody’s. Thousands of companies are rated by these two agencies and their views carry significant weight with financial markets |